Understanding your share of costs

Understanding your share of costs

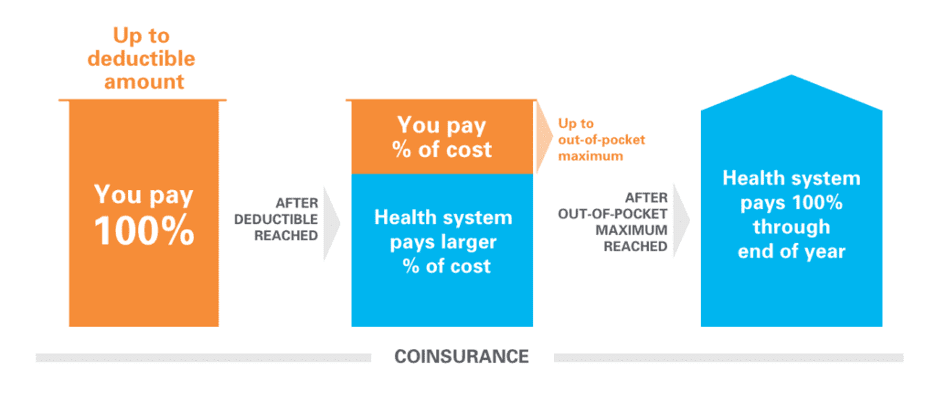

Understanding deductibles, copays and coinsurance

Let’s be honest. The lingo around health insurance is confusing to most people. But, it’s important to understand some key terms so you can choose the medical plan that works best for you and make the most of your coverage during the year.

Spend a few minutes reading this article. Before you dig in, know which health plan you signed up for (HSA Advantage Plan or Signature Plan). You may want to open a second tab and keep the summary of medical plans open so you can refer back to it as you learn about these terms.

When you are enrolled in one of our medical plans, you and the health system share the cost for your healthcare expenses. The health system has engaged Blue Cross Blue Shield to administer our health plans. Prescription coverage is provided as part of both plans with Navitus Health Solutions as the administrator.

Deductibles, coinsurance and copays are examples of your share of costs.

For more information about how you and the health system share the cost for your healthcare expenses on either plan, read Understanding deductibles, copays and coinsurance.

What is a deductible?

A deductible is the amount you pay for the cost of healthcare services and prescriptions you receive before the health system begins to pay its share. Your deductible amount varies based on three factors:

- Which plan you choose (HSA Advantage Plan or Signature Plan)

- Whether you choose coverage for only yourself or yourself and family

- The network your use for facilities and providers (health system, in-network or out-of-network)

How it works: If your deductible is $1,800, you’ll pay 100% of eligible healthcare expenses for care and prescriptions until what you’ve paid adds up to $1,800. After that, you have “met your deductible” and you share the cost with the health system by paying coinsurance for covered services and prescriptions for the rest of the calendar year.

Each medical plan has a different type of deductible. Read about the Signature plan’s embedded deductible and the HSA advantage plan’s aggregate deductible to understand how they work.

What is coinsurance?

Coinsurance is your share of the cost of a covered healthcare service or prescription after you’ve met your deductible. It’s usually figured as a percentage of the amount allowed to be charged for services.

How it works: You’ve paid $1,800 in healthcare expenses and met your deductible. Now when you go to the doctor, instead of paying the full cost, you and the health system share the cost. For example, if you are in the HSA Advantage Plan and go to a specialist physician in the health system network after you’ve met your deductible, the health system pays 90%. The 10% you pay is your coinsurance.

What is a copay?

A copay is a fixed amount you pay for a covered healthcare service or prescription, usually due when you receive the service. The Signature Plan uses copays for many services; the HSA Advantage plan uses copays on a limited basis related to prescriptions for chronic conditions.

The copay amount is different depending on the type of service/prescription and which provider network or pharmacy you use. Copays do not count toward your deductible – you always pay that amount whether you have met your deductible or not until you reach your out-of-pocket maximum.

How it works: You are in the Signature Plan and see a health system specialist several times a year. At each visit, you will pay a $40 copay, even if you have met your annual deductible, until your out-of-pocket maximum is reached.

How each plan works

The HSA Advantage Plan uses coinsurance for all covered services and most prescriptions.

The Signature Plan uses primarily copays for health system and in-network office visits and prescriptions; it uses coinsurance for some services after your deductible is met. Note: Copays do not count toward your deductible.

Preventive care is free in both plans

The health system wants all employees and their families to get the right healthcare services to be well – even if you are already healthy. That’s why the health system pays 100% for preventive care in both plans when you use health system or in-network providers.

That means no deductible to meet and no copay or coinsurance for preventive services. So, don’t delay – keep up with your annual physicals and preventive screening exams.

Embedded vs. aggregate deductibles

The phrase “meet your deductible” means paying that amount before the health system begins to pay its share of your medical care. After you meet your deductible, your share of cost is coinsurance.

Each medical plan has a different type of deductible.

- The Signature Plan uses an embedded deductible.

- The HSA Advantage Plan uses an aggregate deductible.

Both deductibles reset to zero on Jan. 1 each year.

- The Signature Plan has an embedded deductible.

- Once any covered member in your family meets their individual deductible, the health system begins to pay its share for that person’s covered services, even if the family deductible has not been met.

- Example: John has employee + spouse coverage and uses health system providers. They each have an annual deductible of $500.

- John has met his deductible of $500. The health system will now pay a portion of his medical expenses for the rest of this year.

- John’s wife Laurie hasn’t had any medical expenses yet this year but went to a health system emergency room this week. She’ll need to pay the first $500 of the cost since her individual deductible had not been met. Going forward, the health system will pay a portion of qualified expenses for the rest of the year because, with the ER visit, she has met her deductible.

- John and Laurie will continue to pay copays for health system and in-network office visits and prescriptions until their out-of-pocket maximum is met.

- The HSA Advantage Plan has an aggregate deductible.

- The full amount of the family deductible must be met before the health system begins to pay for anyone’s services.

- Example: Steve has employee + spouse coverage and uses health system providers. The family deductible is $3,600.

- In January, Steve went to urgent care, filled prescriptions and had several follow-up doctor’s appointments. His medical bills so far total $1,250.

- Steve’s wife Sarah injured her ankle and had several physical therapy sessions, filled prescriptions and visited her specialist. Her medical bills so far total $2,550.

- Together, Steve and Sarah have met their family deductible, and the health system will pay a portion of their qualified expenses for the rest of this year until their out-of-pocket maximum is met.

- Steve and Sarah used the $1,000 in seed money the health system put in their HSA to pay part of their cost.

What is the out-of-pocket maximum?

This is the most you’ll ever have to pay for covered services/prescriptions in the calendar year. After you’ve paid this amount, you’ll have no copays or coinsurance – the health system will pay 100% of the cost of all covered services and prescriptions for the rest of the calendar year.