Are you paying for care for a child under the age of 13? Or caring for an elderly parent or dependent adult? A child and elder care FSA is a tax-advantaged account that helps you save on your dependent care expenses.

Any benefits-eligible employee can establish a child and elder care FSA – even if you have an HSA or healthcare FSA.

Money you contribute to the account is deducted from your salary before taxes. This deduction reduces your taxable income, saving you money on taxes.

Use the child and elder care FSA to pay for qualified expenses such as preschool, summer day camp and day care for a child or dependent adult. For a complete list of covered expenses, refer to IRS publication 503. Read this overview about child and dependent care FSAs to deepen your understanding.

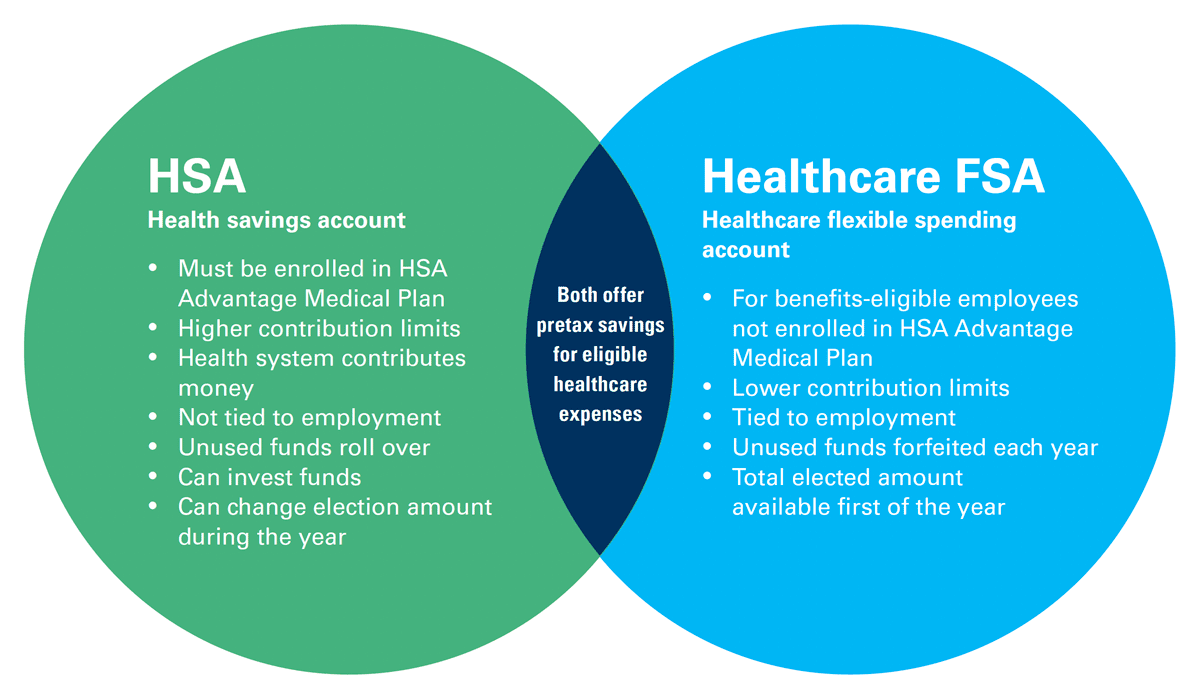

It is an easy and smart way to save money. An HSA pairs with an HSA-eligible medical plan to save on healthcare costs now and invest for future expenses.

Employees who enroll in the HSA Advantage medical plan. Additional IRS requirements are:

More details about eligibility are in this overview about HSAs.

An HSA allows you to save money on a pretax basis to pay for qualified medical expenses for you and your dependents. Think of an HSA as a guaranteed discount on money you’re already going to spend on eligible healthcare expenses (braces, prescription drugs, copays for medical care and much more).

An HSA also can be an effective way to save and invest for future healthcare expenses, such as in retirement.

There are multiple ways to use your HSA for payment or reimbursement of qualified medical expenses, including:

A healthcare flexible spending account (FSA) is a tax-advantaged account that allows you to pay for qualified medical expenses using pretax dollars.

Employees who are not enrolled in the HSA Advantage medical plan but have ongoing or expected medical, prescription, dental and vision costs in the coming year may enroll in a healthcare flexible spending account (FSA). These pretax dollars can also be used for over-the-counter items such as allergy and sinus medications, and first-aid supplies.

Depending on the extent of your healthcare costs, an FSA can help you save a lot of money on taxes.

Read this overview about healthcare FSAs to deepen your understanding.

You can use an FSA debit card to pay upfront, or submit receipts and get reimbursed through Fidelity’s NetBenefits, available online and via a mobile app.

Child and elder care flexible spending account (FSA) Health savings account (HSA) Healthcare flexible spending account (FSA) Who can open the account? Benefits-eligible employees who elect the HSA Advantage medical plan. Benefits-eligible employees who are not enrolled in the HSA Advantage medical plan. Why should I open an account? To save for dependent care expenses expected in 2026. The money you set aside in the FSA is not subject to taxes, so you take home more of your paycheck. To save for future healthcare expenses in 2026 and beyond. Money goes in tax-free, is invested tax-free and can be used to pay for qualified medical, dental and vision expenses. The health system will deposit $500 for individual-only coverage; $1,000 for family coverage. To save for qualified healthcare expenses expected in 2026. The money you set aside in the FSA is not subject to taxes, so you take home more of your paycheck. How can I use the money? To pay for eligible expenses at licensed day or elder care centers, nursery schools, day camps and home care with valid tax ID numbers. To pay for medical, dental and vision expenses including deductibles, coinsurance, prescriptions and other eligible expenses. To pay for medical, dental and vision expenses including deductibles, coinsurance, prescriptions and other eligible expenses. What if I don't use the money in 2026? Any unused funds are forfeited. You have until April 30, 2027, to submit claims for eligible expenses incurred Jan. 1, 2026-Feb. 28, 2027. All unused funds roll over each year. Any unused funds are forfeited. You have until April 30, 2027, to submit claims for eligible expenses incurred Jan. 1, 2026-Feb. 28, 2027. When can I use the money in my account? Money you contribute from each paycheck is available as soon as it's added to your account. Money you contribute from each paycheck is available as soon as it's added to your account. Funds provided by the health system are available in January or, for newly eligible employees, as soon as your account is activated. Your total annual elected amount is available for you to use beginning Jan. 1, 2026. Can I invest the money in my account? No Yes No How much can I contribute? Up to $7,500 as an individual or as a married couple filing jointly; up to $3,750 as a married couple filing separately. Up to $4,400 individual, $8,750 family. Age 55 and over may contribute an extra $1,000. Up to $3,300.